2025 Market Outlook: Crypto, AI, and FTX Recovery Updates

By Mike Abbate, Chief Investment Officer & Jesse Yuan, Senior Research Analyst

January 17, 2025

Key Takeaways

- Crypto and TradFi Converge: The fusion of traditional finance and crypto continues to reshape global markets, bolstered by favorable U.S. policies, spot Bitcoin ETFs, and the evolving regulatory landscape.

- AI Infrastructure Boom: The rapid expansion of AI is driving demand for high-performance data centers, creating new opportunities for Bitcoin miners and reshaping digital infrastructure valuations.

- FTX Recovery Plan: With the effective reorganization of FTX, creditors are set to receive significant distributions, highlighting ongoing shifts in the crypto landscape and investor opportunities.

2025 Outlook

2024 marked an inflection point for the crypto industry, driven by the launch of spot Bitcoin ETFs attracting $58bn of net inflows totalling $108bn of AUM fueled by a favorable monetary policy, the election of a pro-crypto president, an appointment of dedicated crypto/AI czar and most importantly a government agency, focused on reducing the number of government agencies, named after a MEME coin. The irony.

The largest take away of 2024 was the continued fusing of the crypto and tradfi industries so it would not be appropriate to discuss a 2025 outlook for crypto without discussing the outlook for the broader market and economy. The US economy demonstrated incredible resilience in 2024. CPI eased from a peak of 8% in 2022 to 2.5%, while GDP growth stayed strong at 2.8% creating a "goldilocks" environment for asset prices. Despite stock markets making all time highs, the Federal Reserve preemptively initiated a rate-cutting cycle reducing the federal funds rate by 100 basis points over three cuts to 4.5%. We are still scratching our heads as to what data the Fed was watching to prompt these cuts given the Goldman Sachs financial conditions index tracked lower throughout the year while stocks, and bitcoin, made new highs. We will be closely watching the inflationary effects of these rate cuts coupled with the contemplated Trump tariffs, and expected expansionary fiscal policies. While the newly formed Department of Government Efficiency (DOGE) appears to have shifted its focus towards ending US inflation by cutting government overspending, this is no easy task. As a result, we believe the prediction of increased volatility is easier than the continued increase of risk assets broadly.

By far, the most impactful developments on the horizon are the potential regulatory changes under the new administration. With Trump taking office and SEC Chair Gary Gensler stepping down, a major U.S. crypto overhaul is expected. Meanwhile, the EU/s Markets in Crypto-Assets (MiCA) framework, went into effect the end of December 2024, promulgating new rules, which aim to strengthen consumer protections and reduce fraud, among other things. Although this is a step in the right direction, we believe that MiCA may diminish the EU's attractiveness of the jurisdiction for crypto investors and innovators in the near term, especially as the pro-crypto Trump administration takes office. Notably, we believe the delisting of USDT, a critical source of liquidity for many DeFi applications, on EU-based exchanges will make it difficult for EU-based DeFi platforms to efficiently operate given the new barriers to access liquidity, potentially putting them at a disadvantage compared to their global counterparts.

AI Infrastructure

The rapid expansion of AI is driving significant demand for specialized data centers, which have become critical for handling massive computational workloads. Training advanced models requires clustering thousands of high-performance chips, fueling an arms race among tech giants to build and secure infrastructure that can accommodate these ever-growing needs.

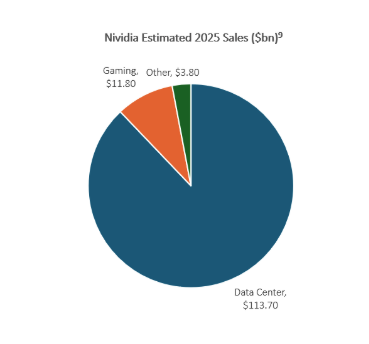

This all costs money, fortunately, mega tech has plenty of it. Microsoft’s plan to invest approximately $80bn to build out datacenters in 2025 exemplifies this shift. This trend is reinforced by Nvidia’s projections that their data center segment will generate over $100bn in sales in 2025. As businesses intensify their reliance on AI across applications, from search engines to enterprise solutions, competition amongst the tech giants will also increase as the need for reliable AI infrastructure grows. We believe digital infrastructure will be the backbone of this progress.

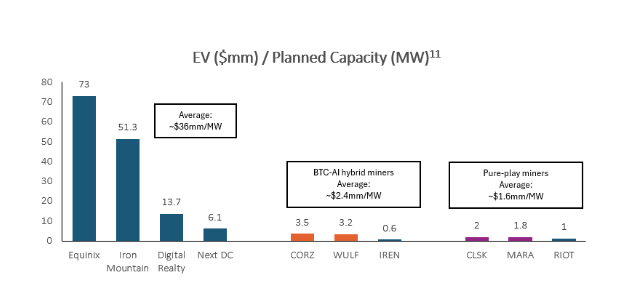

As discussed in our previous memo, Bitcoin miners and AI data centers are increasingly converging around the same finite pool of resources. Following China's 2021 ban on bitcoin mining, the once China-dominated industry saw US miners rapidly expand, securing scalable and energy-efficient power infrastructure. These highly sought-after assets are now equally critical for specialized AI data centers. In fact, some miners diversifying their power portfolios to support AI data centers have significantly outperformed their peers - CORZ (+295%) and WULF (+244%) vs. CLSK (+33%) and RIOT (8%). As bitcoin miners allocate more of their capacity towards AI, we agree with a recent Bernstein report that their EV/MW may trade closer to traditional data center companies, which trade at a 90% premium.

FTX Updates

The FTX Debtors Plan of Reorganization became effective on January 3, 2025. The first distributions will become available for convenience class claim holders within 60 days of the effective date. Convenience class holders should expect at least a 119% recovery on their claim’s petition date value. Separate record and payment dates for other classes of claims will be announced. The two distribution service providers, BitGo and Kraken, are currently available for certain FTX creditors. Distributions will be made in US dollars, and each provider offers different withdrawal methods and fee structures (e.g., wire, ACH, stablecoins, digital assets). Creditors must complete KYC, tax forms, and provider onboarding by specific cut-off dates to receive distributions.